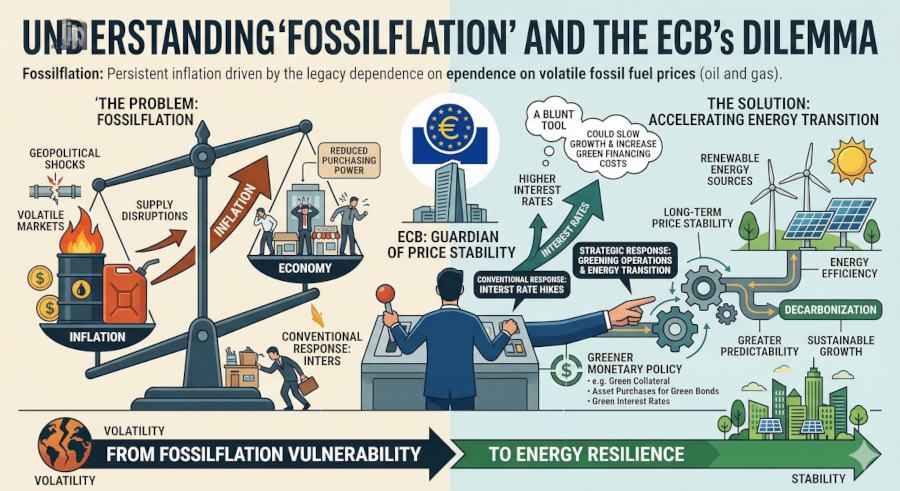

Amid geopolitical tensions and elevated energy prices, central bankers face a difficult choice: tighten policy to crush energy-driven inflation, or hold steady to protect investments in the energy transition?

As the conflict in the middle east continues and with no sign of a possible appeasement, pressure will be mounting in the coming weeks on central banks to adjust their monetary policy course. The ECB’s governing council is meeting exactly today and this issue will obviously be on their minds.

This is a debate we had back in 2022: the “team transitory” position was that the ECB should not intervene, arguing that the post-COVID inflation would naturally subside. However, the shock of the war in Ukraine clarified that the inflationary impact from the disruption in gas markets would be much greater than initially anticipated.

Already yesterday Chris Giles argued in the Financial Times that central banks must actively prevent persistent inflation and wage-price spirals, stemming from higher fuel prices, through a credible commitment to policy tightening.

While major ECB decisions are unlikely this week, I hope the lessons of 2022-2023 are learned. As a modest attempt to contribute to this debate, I will review in this article some of the recent literature on the implications of energy price shocks for monetary policy implementation.

Yes, central banks can actually lower energy prices

Contrary to what I thought a few years ago, monetary policy tightening, if frontloaded, can effectively help lower prices. Gökhan Ider , Alexander Kriwoluzky , Frederik Kurcz and Ben Schumann (2024) demonstrate that the optimal mandate-achieving policy involves a front-loaded tightening, particularly at the longer end of the yield curve, which quickly depresses global energy prices and stabilizes inflation expectations without inducing a severe recession.

BUT…

However while their analytical conclusion might be correct, many economists would disagree with the policy prescription. For instance Veronica Guerrieri, Michala Marcussen , Lucrezia Reichlin and Silvana Tenreyro (2023) have argued for patience. They show that energy supply shocks affect sectors asymmetrically, requiring temporary higher inflation to facilitate efficient resource reallocation and relative price adjustments.

Adding to this perspective, Gregor Boehl, Flora Budianto, and Előd Takáts (2024) show in this BIS paper that a monetary policy with less emphasis on strict inflation stabilization actually accelerates the green transition, as temporarily higher inflation and energy prices boost clean innovation. In the same vein, David Barmes , Irene Claeys, Simon Dikau and Luiz Awazu Pereira da Silva (2024) advocate for an “adaptive inflation targeting” framework.

Going further Luca Fornaro , Veronica Guerrieri, and Lucrezia Reichlin (2025) have acutely explained how the central bank’s “reaction function” is fundamentally complicated by the “green dilemma” : hiking rates during an energy crisis may help tame inflation on the short-run, but could structurally damage the long-term green transition. In particular, higher cost of capital is particularly harmful for investments in the green technologies that we actually need to get rid of our fossil fuel dependencies and make the economy more resilient against the very type of shocks that we are seeing today.

This hypothesis is empirically confirmed by Alexandra Serebriakova, Friedemann Polzin and Mark Sanders (2026). In a very recent paper published in Energy Economics, they find that over 2001–2024, every 25 basis point increase in policy rates by the ECB have reduced installed capacity for onshore wind by 3.2 percent and solar photovoltaic by 5.3 percent, equivalent to a decrease in renewables energy by 0.16% in the EU’s energy mix.

A complementary study by Daniel Navia Simon, and Laura Diaz Anadon (2025) projects that if member states achieve their climate and energy plans by 2030, the overall EU electricity price would fall by at least 26%. However the literature is very nuanced as to what extend cheaper renewable energy generation may translate into lower HICP inflation. For instance, in this IMF working paper, Laurent Millischer, Chenxu Fy, Ulrich Volz and John Beirne (2024) find no correlation, while Łukasz Markowski and Kamil Kotliński (2023) find a small one (1pp additional renewable lead to -0.13% inflation).

So what?

Finding the optimal monetary policy response in a context of energy price shocks is a complex issue. As I have extensively written elsewhere, I have a personal preference for the introduction of differentiated interest rates (see my WWF report here) as a solution to the green dilemma: if it needed to, the ECB could raise its key interest rates, while maintaining lower rates under refinancing operations targeted at specific loans for renewables and energy efficiency .

But leaving such innovative policy option aside, a more general implication of the recent literature is that the discussion must extend beyond simply how the ECB can best achieve 2% inflation in the medium term. Central banks must also consider the costs involved for society and the expected outcome on the economy after the crisis is gone.

Just like Trump should not have made reckless moves to attack Iran without a clear endgame in mind, central banks should avoid hastily raising rates in the short term if they can predictably see how the economy would be more vulnerable and less competitive as a result.